TORONTO – Canadians took out fewer new mortgages even before interest rates began to rise last week, but consumer debt continued to increase in the fourth quarter, Equifax said in a report.

The company said Monday the number of new mortgages fell 8.1 per cent year over year in the last three months of 2021. The biggest drop was in some of the country’s hottest housing markets with Toronto and Hamilton falling 16.1 and 18.7 per cent, respectively.

“There’s no question that skyrocketing house prices have decreased housing affordability across all segments,” said Rebecca Oakes, assistant vice-president of advanced analytics at Equifax Canada in a news release.

“In addition to high house prices, lenders have also started to move interest rates up in anticipation of rate rises from the Bank of Canada. This could also be limiting the purchasing capacity of many consumers.”

The Bank of Canada hiked its benchmark rate by a quarter of a percentage point to 0.50 per cent last week with more increases expected later this year.

The average new mortgage loan increased 10.1 per cent from the fourth quarter of 2020 to $355,000, but dropped 1.5 per cent from the third quarter for the first decrease since the pandemic began.

Oakes said this may be a sign of average home prices stabilizing, although continued demand and lack of supply could lead to further rises in the property prices.

Source: Equifax Canada

Source: Equifax CanadaEquifax also says total consumer debt rose 7.9 per cent compared with a year earlier to $2.2 trillion as credit card spending in the fourth quarter was up 14.4 per cent from a year earlier and up 9.8 per cent from the third quarter.

Consumers spent an average of $2,205 per month on their cards in the fourth quarter, up 15.2 per cent from the year-ago period and 6.8 per cent above the pre-pandemic level in the fourth quarter of 2019.

“The holiday period always leads to an increase in spending, but Q4 2021 saw higher than ever average credit card spending per credit card consumer,” said Oakes.

A drop in auto loans because of supply chain issues was a positive contributor.

Equifax said overall credit card balances were up 2.4 per cent compared with the fourth quarter of 2020.

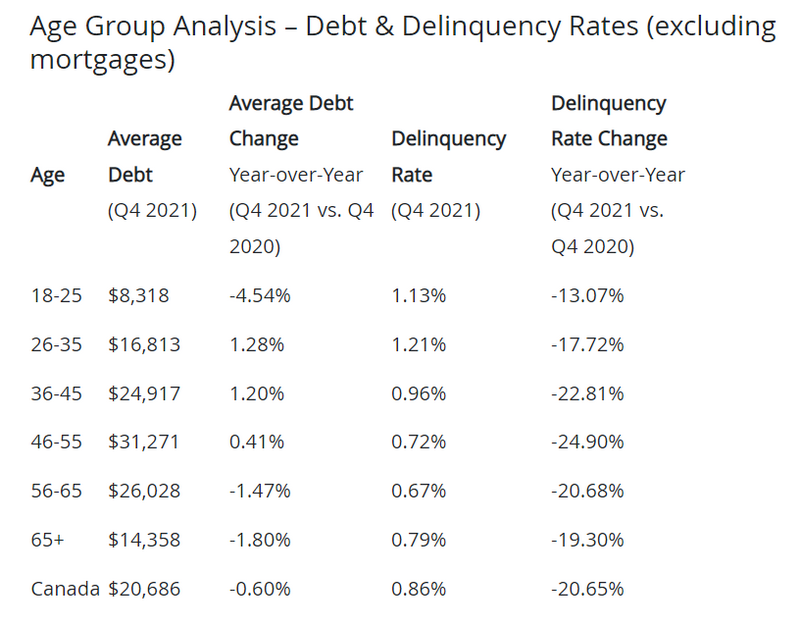

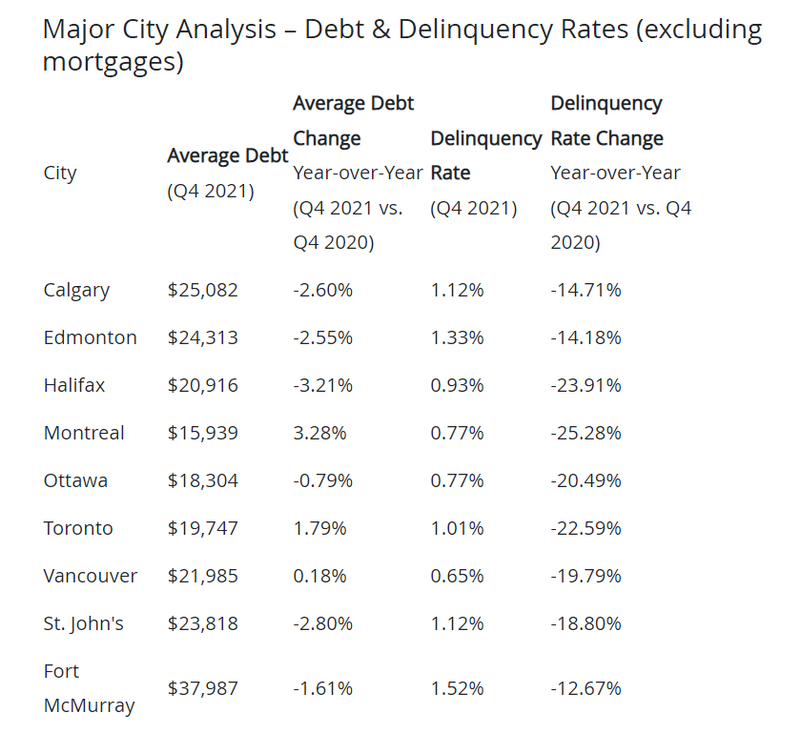

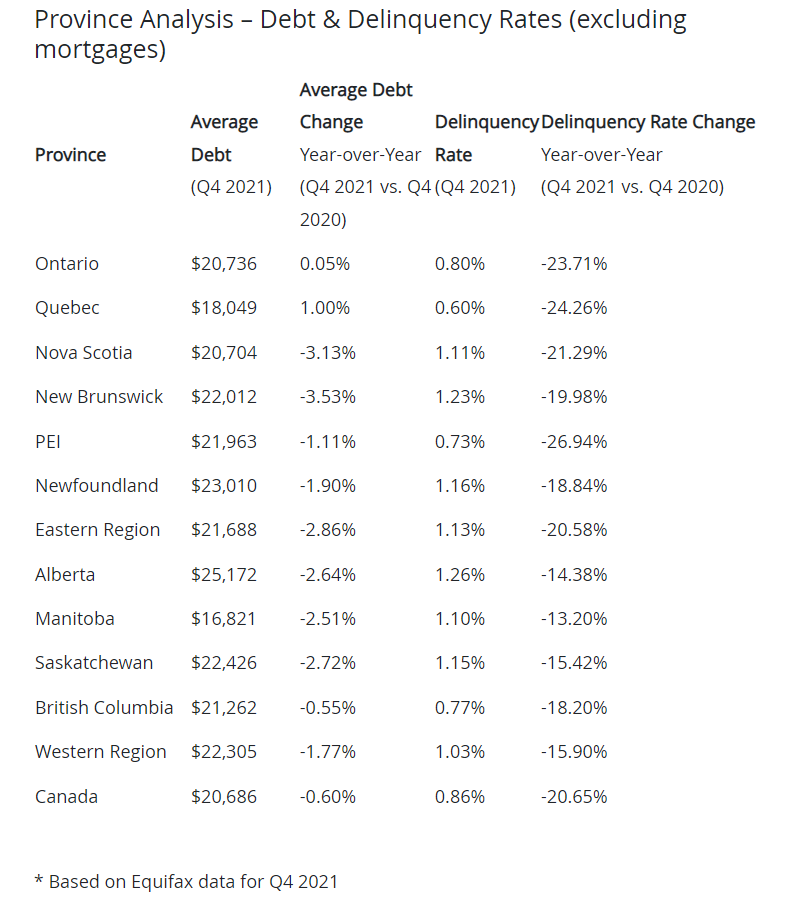

Overall delinquencies remained low with mortgage delinquency at 0.11 per cent and non-mortgage delinquency at 0.86 per cent, for year-over-year drops of 31.8 per cent and 20.7 per cent, respectively.

Terminations last 4 weeks, 416 freeholds:

Feb 13: 58

Feb 20: 79

Feb 27: 83

Mar 6: 111Def up. But there’s way more new listings coming on line now so sales and active listings are up >500 in that time. Still, higher than most years at this time. /2 pic.twitter.com/bxSsB1K2z0

— Scott Ingram CPA, CA (@areacode416) March 7, 2022

But I wouldn’t say a couple of weeks of 4% increases is conclusive. The straight climb at the beginning of the pandemic was conclusive, and the 19% jump in one week after Ont Fair Housing Plan in 2017 was convincing too. /4

— Scott Ingram CPA, CA (@areacode416) March 7, 2022

Now the Terminations % is more in line with seasonal averages as opposed to at new lows. I keep comparing back to 2017 because my guess (and we’re all just guessing) is this market is going to play out a lot like 2017. /6 pic.twitter.com/Pu6gkGVtuH

— Scott Ingram CPA, CA (@areacode416) March 7, 2022

This is the only chart I have that contradicts the narrative above. But this stat is just on the ones that actually sold, so don’t tell the whole story (i.e. re-listings).

It’s like a going 150 km/h and slowed to 140 km/h thing at this point. But starts somewhere. /8 pic.twitter.com/NlMUZqq7Dv

— Scott Ingram CPA, CA (@areacode416) March 7, 2022

In fact I do! 🤓I update it on Tuesdays when I look at Active Listings.

Both ownership types are up from bottom (8.8% vs. 7.6% for freehold, 8.7% vs. 7.0% for condo), so appears a little bit of something but freehold actually down (10.0% > 8.7%) in last couple. Will relook tmrw pic.twitter.com/BFhMTj6S15

— Scott Ingram CPA, CA (@areacode416) March 7, 2022

Homes Are Selling But….

But for the last 3 weeks the level of multiple applicants on mortgages to get the application to qualify has gone through the roof

3 people, 4 people maybe more

Used to be Drive till you qualify, now it’s add family co-signers till you qualify

— Ron Butler (@ronmortgageguy) March 3, 2022

The earliest signs of a slowdown in the housing market can be seen in micro trends like this

It’s interesting how real estate agents have become the source for real time insights into the housing market

If this trend continues, we might see it in the aggregate data by May/June https://t.co/31uLudO3BL

— John Pasalis (@JohnPasalis) March 6, 2022

Oh: and we’re just coming into the 3rd year of a multigenerational health and economic event. Plus a decade of an interest rate-driven consumer debt & housing bubble.

— Scott Terrio (@ScottTerrioHMA) March 4, 2022

What happens when you put 10 economists in a room? You’ll get 11 opinions

An old joke, but we can see this today in the wide range of opinions about Toronto’s housing market

This note from BMO’s Robert Kavcic lines up with how I see the market today https://t.co/otRN43TYo7

— John Pasalis (@JohnPasalis) March 5, 2022